The CRA was asked a question regarding the application of Part IV tax and the determination of the timing when a corporate beneficiary of a trust receives a dividend designated under subsection 104(19) of the Income Tax Act (Canada) (the "Act").

The facts presented were as follows:

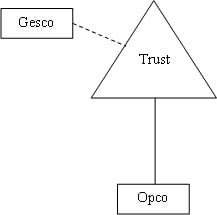

- Opco and Gesco are both SPCCs;

- Opco is wholly-owned by Trust;

- Opco has a May 31st year-end;

- Gesco and Trust have December 31 year-end;

- On May 31st, Opco pays a $10,000 dividend to Trust;

- On May 31st, Trust distributes said amount to Gesco pursuant to subsection 104(19) of the Act;

- Opco does not receive any refund of RDTOH for the year;

- On May 31st, Opco and Gesco are "connected" pursuant to paragraph 186(4)(a) of the Act; and

- On June 1st, Trust sells all shares of Opco to non-related third party.

The CRA concluded that given the hypothetical facts, Part IV tax would be payable by Gesco on the $10,000 dividend received from Opco pursuant to subsection 104(19) of the Act.

Amongst the conditions of application of subsection 104(19), the trust must be resident in Canada throughout the year and an amount must be attributed to a taxpayer by the trust in its year-end tax returns. Accordingly, it is the CRA's position that an amount received by a beneficiary of a trust pursuant to 104(19) of the Act cannot be deemed a dividend received by said beneficiary until the trust's year-end. This is based on the rationale that the determination of a trust's residency throughout the year as well as the attribution itself cannot be made by prior to the trust's year-end. Furthermore, the CRA notes that the determination of whether an assessable dividend was received from a "connected" corporation must be made at the time that the dividend was received.

Given the foregoing, the CRA concluded that Gesco would be deemed to receive the dividend as of December 31st, at which point in time Opco and Gesco would no longer be "connected" corporations as a result of the sale by the Trust of all its shares of Opco to a non-related third party. Consequently, Gesco would have to pay Part IV tax on the dividend attributed to it pursuant to 104(19) of the Act. The CRA also stated that its conclusion is equally applicable in the alternative where the Trust distributes the $10,000 to Gesco on June 30th rather than May 31st".